Welcome back — and welcome to the first newsletter of 2026.

Last year was a strong one. That’s worth acknowledging — briefly. Navigating a tumultuous 2025 required discipline, and the system did its job. Now it’s time to get back to work refining what got us there.

The past year was a reminder that markets rarely move in isolation.

While much of the focus remained on US equities and mega-cap technology, 2025 quietly turned into a broad global advance. Returns were strong across regions — just not always where headlines suggested.

Understanding that distinction — between what the market looked like and what it actually was — matters as we move into 2026.

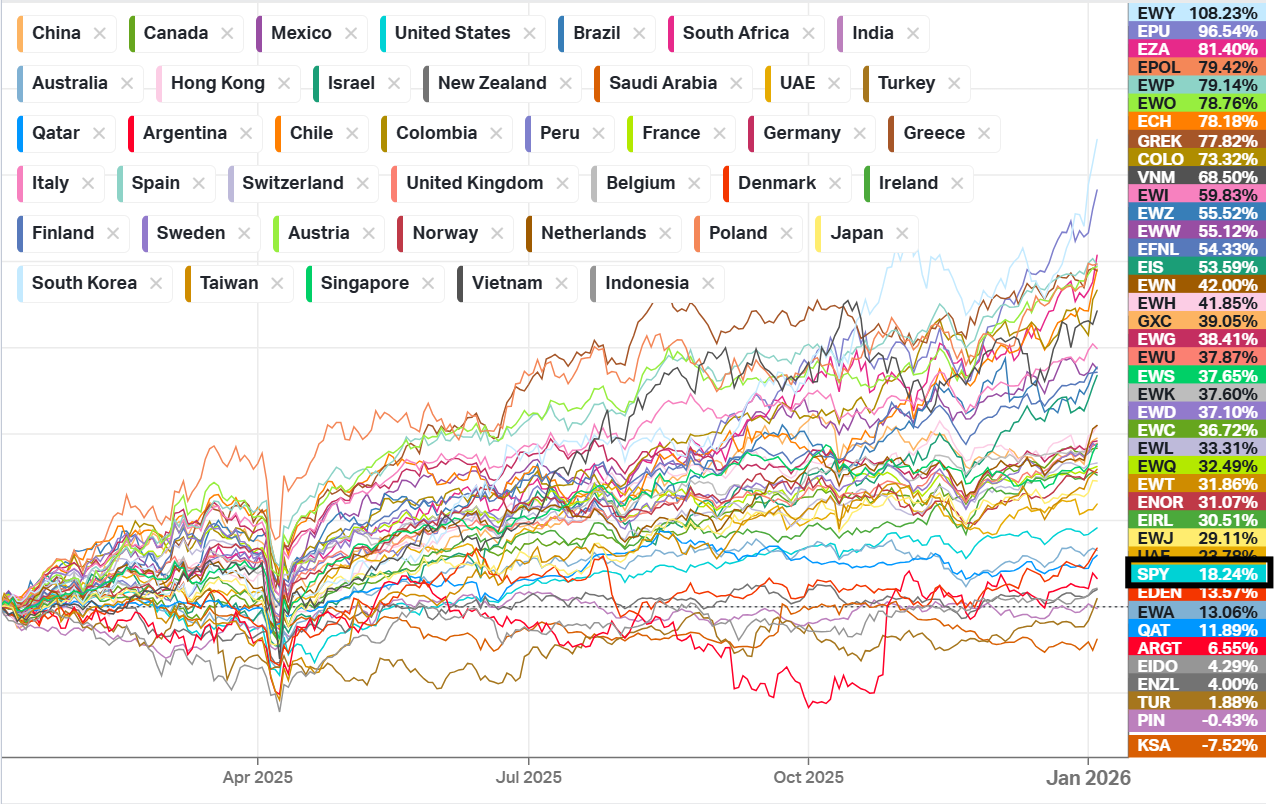

The Entire World Was a Bull Market

There’s a common perception that the benchmark to beat for annual returns is somewhere in the 8–10% range on the S&P 500, depending on who you ask.

But the idea of an “average year” isn’t so average.

In fact, since 1950, the S&P has only delivered returns in that range four times. Most years are meaningfully better — or meaningfully worse. Last year was no different. The S&P finished 2025 up 17.72%, which is a strong result by any historical standard — especially considering the year included a 15.03% drawdown during the tariff tantrum.

So yes, 2025 was a good year for US equities.

What I find far more interesting, however, is where that return stacks up to markets around the world.

A Global Rally Hiding in Plain Sight

I deliberately made this chart look like a coloring book to drive the point home.

2025 wasn’t just a US bull market — it was a global bull market.

These figures represent trailing 12-month returns as of January 2026 but the takeaway is clear. What many investors would consider a great year for the S&P 500 turns out to be only good enough for the bottom of the pack globally.

Given the daily barrage of geopolitical headlines, economic uncertainty, and regional risks, this often comes as a surprise.

And if you’re like me, the next question is obvious:

What was driving returns everywhere else?

Different Markets, Different Engines

It’s no secret that the US stock market is dominated by large-cap technology. What’s less appreciated is just how unique that structure is compared to most markets around the world.

Outside the US — and excluding markets like Canada and South Korea — equity indices look very different. Globally, many markets are dominated not by technology, but by materials, industrials, and financials.

In developed markets outside the US:

- Financials make up roughly 25% of index composition

- Industrials account for about 19%

Latin America provides an even clearer example. It was one of the strongest-performing regions in 2025, and its equity index is composed of roughly:

- 40% Financials

- 21% Materials

These sectors don’t dominate headlines. But they dominated returns.

A Quiet Strength Across Global Markets

That strength is showing up in more ways than just annual returns:

- The Eurozone Top 50 Index recently set new all-time highs

- Spain reached 18-year highs

- Italy reached 18-year highs

- European financials hit 11-year highs and are on the verge of a relative performance breakout versus US financials

These are not fringe markets. And these moves didn’t happen overnight.

They happened quietly — beneath the surface.

The Tactical Takeaway

The point here isn’t to abandon US markets or mega-cap technology.

It’s this:

If your attention is consumed by concentration risk in a handful of names, it becomes easy to miss other powerful trends developing in plain sight.

Explanations always come later. Trends don’t wait for consensus, and they rarely arrive with a clear narrative attached. A declining dollar may help explain parts of this move — but tactical investing isn’t about debating why something should be happening. It’s about recognizing what is happening.

There is never a shortage of good opportunities in markets. The challenge is identifying the best ones early — before they become obvious, crowded, or fully explained.

That’s where a disciplined, system-based process matters. It cuts through the noise, weighs the evidence objectively, and keeps decision-making grounded in price, participation, and relative strength — not headlines.

That’s how leadership is identified early.

And that’s the work as we move into 2026.

The views stated in this letter are not necessarily the opinion of Cetera Wealth Services, LLC, and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not take into account the effects of inflation and the fees and expenses associated with investing.