Market leadership remains a central theme as we move deeper into the fourth quarter. Two dynamics are defining this environment: deteriorating breadth and technology’s unrelenting leadership. While both may sound at odds, together they tell a story of a market that’s become more selective, not necessarily more fragile.

Breadth Deterioration — What’s Really Happening Beneath the Surface

Since peaking in late March, market breadth has been steadily weakening across the major indexes, a trend that accelerated through October. The gap between capitalization-weighted and equal-weighted versions of the S&P 500 and Nasdaq has widened considerably. This divergence has reignited conversations about concentration risk, as the largest companies in the index continue to shoulder most of the market’s gains.

However, it’s worth reframing this concern. Imagine the opposite scenario—what if the largest, most liquid, and growth-oriented companies weren’t performing well? That would pose a far greater threat to market stability. In reality, what we’re seeing is a consolidation of leadership, not a breakdown of participation. The top names are doing what true leaders should: delivering strong earnings, showing margin resilience, and supporting the broader market during periods of rotation and uncertainty.

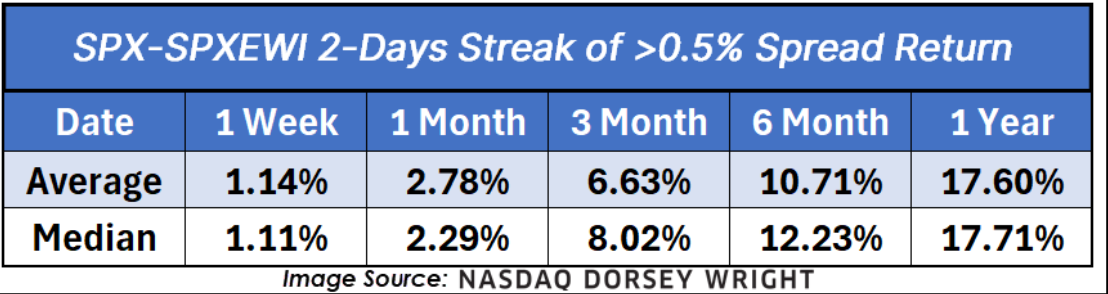

Recent research from Dorsey Wright helps illustrate this point. They found that periods where the cap-weighted S&P 500 outperforms the equal-weight version by more than 0.5% for consecutive days—as has happened recently—have historically preceded strong forward returns. In other words, leadership concentration often reflects confidence and momentum, not instability. The market is simply directing capital toward what’s working.

Technology’s Dominance — Clear, Rational Leadership

From a sector-level view, we remain in a technology-led market. The relative performance ratio of Technology versus the S&P 500 continues to press into new highs, reaching levels last seen in 2000. Over the trailing 30 days, Technology (+3.24%) stands as the only sector outperforming the S&P 500’s +0.90% gain, underscoring how concentrated leadership has become.

On a year-to-date basis, Technology (+27.01%) has emerged as the clear leader among the four sectors still ahead of the index, outpacing Utilities (+19.82%), Communications (+17.56%), and Industrials (+17.01%), compared with the S&P 500’s +16.22%. The data confirm what price action has been signaling for months — leadership is both persistent and decisive.

Recent earnings have reinforced this leadership trend, with strong results across the Magnificent Seven—aside from Meta—further validating large-cap growth as the market’s core leadership engine.

Much of the breadth deterioration has come from weakness in defensive sectors — Consumer Staples, Real Estate, and Materials have been among the laggards, while Communications’ softness largely reflects Meta’s post-earnings reaction. This narrowing participation isn’t signaling risk aversion; it’s showing where strength is consolidating. As long as this remains orderly underperformance rather than capitulation, the broader trend structure stays intact — with Technology continuing to anchor market leadership.

Interpreting the Signal — Focused, Not Fragile

Breadth deterioration is best viewed as a warning light, not a red flag. Narrowing participation can evolve into renewed broad strength if underlying leaders remain constructive—and right now, they do. The critical question from here is whether technology eventually pauses long enough for other sectors to catch up, or whether the laggards close the gap on their own. Either outcome would mark a healthier, more sustainable phase of the bull market.

That said, some near-term volatility should be expected as this process unfolds. With leadership stretched and sentiment leaning heavily toward growth and tech, a pullback wouldn’t break trend—it would reinforce it. Both technology and other offensive sectors have room to retrace while remaining within their broader uptrends.

For active managers, this environment offers clarity. With leadership so clearly defined, the “pond we fish in” for outperformance has become smaller but deeper. The task now is to stay aligned with where relative strength resides—currently, that’s in technology and large-cap growth—while staying nimble enough to identify early signs of rotation.

Closing Thoughts

Breadth deterioration doesn’t always mean weakness; sometimes, it means efficiency. The market is speaking clearly about where conviction lies, and for now, that conviction lives squarely in the technology and growth complex. As long as leadership remains resilient and defensive softness stays orderly, the current regime favors focus over fear.

In short: follow the strength, stay adaptive, and let leadership lead.

In a market defined by focused leadership, clarity is an advantage. If you’d like to see how I’m positioning portfolios to capture current strength while preparing for rotation ahead, let’s schedule a time to talk.

The views stated in this letter are not necessarily the opinion of Cetera Wealth Services, LLC, and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.